Here’s something that’ll blow your mind: the way fintech companies decide whether to lend you money is getting a serious upgrade. And I’m not talking about minor tweaks to old formulas — I’m talking about reinforcement learning algorithms that literally learn from every lending decision they make.

Scikit-learn Cross Validation: Master K-Fold and Stratified Techniques

on

Get link

Facebook

X

Pinterest

Email

Other Apps

Remember that time you built a model with 98% accuracy on your test set, deployed it with confidence, and then watched it completely faceplant in production? Yeah, me too. Turns out I’d gotten ridiculously lucky with my train-test split, and my model had basically memorized noise instead of learning patterns.

That’s when I finally understood why everyone keeps harping about cross-validation. It’s not just some academic best practice — it’s your insurance policy against embarrassing yourself with overfit models. Let me show you how to actually use scikit-learn’s cross-validation tools properly, because the docs are technically correct but practically confusing.

Scikit-learn Cross Validation

Why Your Train-Test Split Is Lying to You

Here’s the uncomfortable truth: a single train-test split is basically gambling. You’re making huge decisions based on one random sample of your data. What if your test set happened to be easier than average? Or harder? You’d never know.

I once built a customer churn model where my test set accidentally contained mostly long-term customers. The model looked great — until we deployed it and realized it sucked at predicting churn for new customers. Oops.

Cross-validation fixes this by testing your model on multiple different splits. You get a much more honest assessment of how it’ll actually perform. No more lucky accidents skewing your perception.

The core problems it solves:

Reduces variance in performance estimates

Uses all your data for both training and validation

Catches overfitting you’d miss with a single split

Gives you confidence intervals on your metrics

Reveals if your model is unstable across different data samples

Think of it like this: would you rather make a major decision based on one coin flip, or a hundred? Yeah, that’s cross-validation.

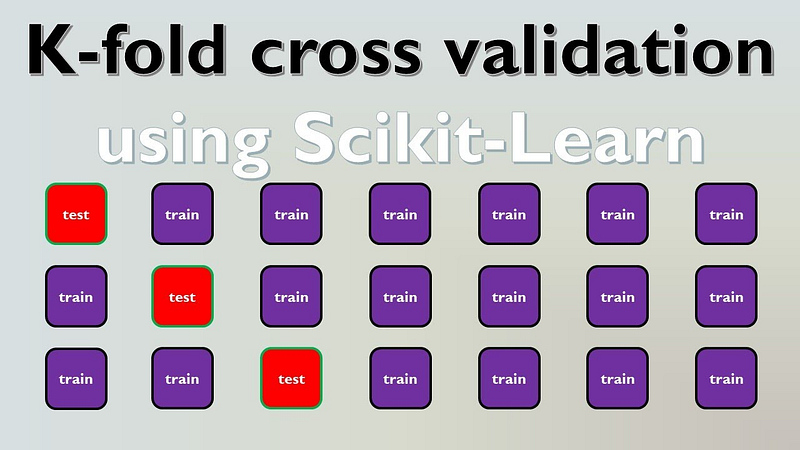

K-Fold Cross-Validation: The Foundation

K-Fold is your bread-and-butter technique. It splits your data into K equal chunks (folds), trains on K-1 folds, and validates on the remaining fold. Repeat K times, rotating which fold is the validation set.

The Basic Implementation

Scikit-learn makes this almost too easy:

python

from sklearn.model_selectionimportcross_val_score from sklearn.ensembleimportRandomForestClassifier

model = RandomForestClassifier() scores = cross_val_score(model, X, y, cv=5)

That’s it. You’ve just trained and validated your model five times across different data splits. The scores array contains performance for each fold.

Understanding the K Parameter

People always ask: “What K should I use?” The standard answer is 5 or 10, but let me give you the real answer: it depends on your dataset size.

Choosing your K value:

K=5: Good default for medium datasets (1,000–10,000 samples)

K=10: Better for smaller datasets where you need more training data per fold

K=3: Faster for huge datasets where 5-fold takes forever

K=N (Leave-One-Out): Only for tiny datasets under 100 samples

I typically start with K=5 because it’s fast and gives reliable estimates. If results seem noisy, I bump it to 10.

The Performance Trade-off

Here’s something nobody mentions: K-Fold gets expensive fast. Training 10 models instead of 1 means 10x the computation time. For deep learning or huge datasets, that’s a problem.

My rule of thumb? Use K-Fold during model selection and hyperparameter tuning. Once you’ve picked your approach, a simple train-test split for your final validation is often fine.

Stratified K-Fold: When Class Balance Matters

Regular K-Fold has a sneaky problem with imbalanced datasets. If you’ve got a fraud detection problem where 99% of transactions are legitimate, random splitting might give you folds with zero fraud cases. Your model trains on nothing, learns nothing, and you wonder why everything broke.

Enter StratifiedKFold — it ensures each fold maintains the same class distribution as your original dataset.

Why This Saved My Bacon

I was building a medical diagnosis classifier with 85% negative cases and 15% positive. Regular K-Fold gave me wildly inconsistent results — some folds had almost no positive cases. Switched to StratifiedKFold, and suddenly my metrics stabilized.

python

from sklearn.model_selectionimportStratifiedKFold, cross_val_score

IMO, just default to StratifiedKFold for classification. The overhead is negligible, and it prevents nasty surprises.

Cross-Val Score vs Cross-Val Predict: Know the Difference

This confused me for way too long. Scikit-learn has cross_val_score and cross_val_predict, and they're not interchangeable.

Cross-Val Score for Quick Metrics

cross_val_score returns performance scores for each fold:

python

from sklearn.metricsimport make_scorer, f1_score

# Get accuracy by default acc_scores = cross_val_score(model, X, y, cv=5)

# Or specify a different metric f1_scorer = make_scorer(f1_score, average='weighted') f1_scores = cross_val_score(model, X, y, cv=5, scoring=f1_scorer)

Fast, clean, perfect for comparing models. But you don’t get the actual predictions.

Cross-Val Predict for Detailed Analysis

cross_val_predict returns the actual predictions for each sample:

python

from sklearn.model_selectionimport cross_val_predict from sklearn.metricsimport confusion_matrix, classification_report

predictions = cross_val_predict(model, X, y, cv=5)

# Now you can do detailed analysis print(confusion_matrix(y, predictions)) print(classification_report(y, predictions))

Use this when you need to understand what your model is getting wrong, not just how often it’s wrong.

Quick decision guide:

Comparing models? → cross_val_score

Debugging predictions? → cross_val_predict

Need both? → Run them separately

Advanced Cross-Validation Techniques

Once you’ve mastered the basics, there are specialized splitters for tricky situations.

Repeated K-Fold: Reducing Randomness

Ever noticed that K-Fold results change slightly each time you run it? That’s because the random split affects everything. RepeatedKFold runs K-Fold multiple times with different random states and averages the results.

python

from sklearn.model_selectionimportRepeatedStratifiedKFold

Now you’ve trained 50 models (5 folds × 10 repeats), and your performance estimate is rock solid. Also slow as molasses, but accurate.

Group K-Fold: Preventing Data Leakage

Got multiple samples from the same source? Like patient records over time, or multiple images from the same camera? GroupKFold ensures samples from the same group never split across train and test.

python

from sklearn.model_selectionimportGroupKFold

groups = [1, 1, 1, 2, 2, 2, 3, 3, 3] # Patient IDs or similar gkf = GroupKFold(n_splits=3)

for train_idx, test_idx in gkf.split(X, y, groups): # All samples from group 1 are together X_train, X_test = X[train_idx], X[test_idx]

Prevents cheating where your model learns patient-specific patterns instead of generalizable features. Critical for medical, financial, or any hierarchical data.

TimeSeriesSplit: Respecting Temporal Order

Time-series data breaks all the rules. You can’t randomly shuffle because that creates impossible “future predicting past” scenarios. TimeSeriesSplit respects time order.

python

from sklearn.model_selectionimportTimeSeriesSplit

tscv = TimeSeriesSplit(n_splits=5)

for train_idx, test_idx in tscv.split(X): # Training data always comes before test data X_train, X_test = X[train_idx], X[test_idx]

Each split uses an expanding window — more training data with each fold. Mimics how you’d actually deploy a time-series model.

Hyperparameter Tuning with Cross-Validation

Cross-validation really shines during hyperparameter tuning. GridSearchCV and RandomizedSearchCV use cross-validation internally to evaluate each parameter combination.

You just trained your scaler on the entire dataset, including the validation folds. Information leaked from test to train. Your scores are optimistic lies.

The right way:

python

# CORRECT - preprocessing inside CV from sklearn.pipeline importPipeline

Now scaling happens separately for each fold. No leakage, honest results.

Mistake 2: Using K=N on Large Datasets

Leave-One-Out Cross-Validation sounds appealing — maximum training data per fold! But on a 10,000-sample dataset, you’re training 10,000 models. Your laptop will hate you.

I tried this once. The script ran for 6 hours before I killed it. Stick with K=5 or K=10 unless your dataset is tiny.

Mistake 3: Ignoring Computational Cost

Cross-validation is expensive. Deep learning models, large datasets, or complex pipelines can make K-Fold impractical. FYI, a single fold taking 10 minutes means 5-fold CV takes nearly an hour.

Speed optimization tricks:

Use smaller K for initial experiments

Implement early stopping in iterative models

Sample your data for quick tests

Save trained models to avoid re-training

Use n_jobs=-1 for parallel processing

Putting It All Together: A Real-World Example

Here’s how I typically structure model evaluation:

python

from sklearn.model_selectionimportStratifiedKFold, cross_validate from sklearn.pipelineimportPipeline from sklearn.preprocessingimportStandardScaler from sklearn.ensembleimportRandomForestClassifier from sklearn.metricsimport make_scorer, precision_score, recall_score, f1_score

This gives you a comprehensive view: multiple metrics, training vs validation performance (for spotting overfitting), and confidence intervals.

The Cross-Validation Mindset

Here’s what finally clicked for me: cross-validation isn’t about getting better models — it’s about making better decisions. That single test score isn’t gospel. It’s one data point with uncertainty.

Use cross-validation to understand that uncertainty. Is your model consistently good, or does it wildly vary? Are you actually improving performance with that fancy feature engineering, or just getting lucky with random splits?

The best part? Once you’ve got cross-validation in your workflow, you’ll catch so many problems before they hit production. Models that looked great but were actually overfit. Feature engineering that seemed clever but didn’t generalize. Hyperparameters that worked on your test set but nowhere else.

Start with simple 5-fold StratifiedKFold. Build it into your evaluation pipeline. Let it become automatic. Your deployed models will thank you — and more importantly, so will your users who won’t deal with garbage predictions.

Now go forth and validate properly. Your future self will appreciate it when that 98% accuracy score holds up in production. 🙂

Comments

Post a Comment